A garnishee order is an action that allows a creditor to bypass you and go straight to your employer, bank or financial institution (with whom you have accounts) to recover a debt you owe.

If this happens, your bank or financial institution may be directed to withhold the money in your bank accounts or your employer may be instructed to withhold wages from you.

If you’ve received a garnishee order, it’s important to do something as quickly as possible.

How does a garnishee order work anyway?

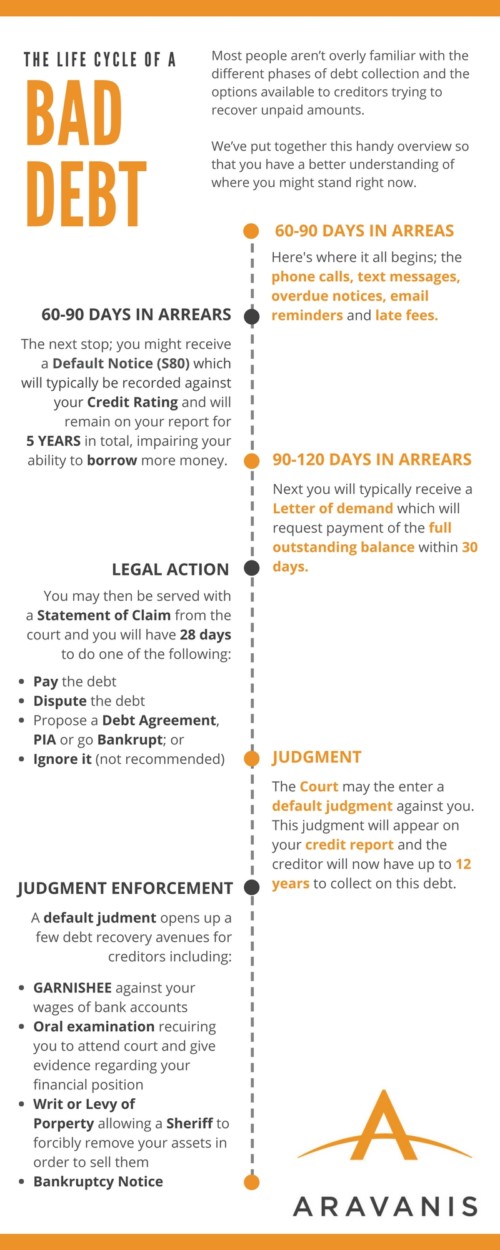

A judgment debt usually occurs when a debt goes unpaid, you’ve been unable to come to agreements with the creditor, and they’ve otherwise exhausted alternative debt collection avenues.

Once a creditor obtains a default judgment, it opens up new legal avenues for the creditor when trying to collect the amount owed. A garnishee order is just ONE of those legal avenues.

You won’t be served the order personally, rather, it’ll be served on third parties – such as the company you work for, the institution you bank with or other third parties who might owe you money. Once the order is made and served on your employer, financial institution or other third parties, they have no choice but to comply with the garnishee orders made by the court.

A garnishee order made to your employer

If a garnishee order for debts is served on your employer, they will withhold and redirect amounts from your pay to the judgment creditor. A garnishee order against wages/income will continue until the judgment debt is paid in full, the court orders the garnishee be discontinued, or some other legislation comes into effect that can stop the order – such as the Bankruptcy Act.

It’s important to know that your employer will not withhold all of your wages. At law, a debtor’s employer will need to retain a certain amount from a debtor’s wages for them to live on, sometimes known as a weekly compensation amount. In some states, the minimum amount can be as little as $495 per week.

If the order will leave you in an untenable situation, it’s best to seek help or legal advice immediately.

A garnishee order made on your bank accounts

When a creditor does successfully apply for a garnishee, the order can also be served on banks and financial institutions as an alternative to seeking a garnishee against wages or salary. Generally speaking, the institution may freeze a judgment debtor’s bank accounts. If this happens, they may also deduct the full amount owing to the judgment creditor in one payment (depending on your available funds).

A garnishee order made against other third parties who owe you money

A garnishee order for debt can also be made against third parties who owe money to the debtor. The order issued is usually for a lump sum of money, rather than ongoing payments and these third parties could be contractors, tenants, or any other party that owes the debtor money.

Can the ATO issue garnishee orders too?

Yes. Additionally, the ATO doesn’t need to seek an order from the court to issue and enforce a garnishee. The Tax Act empowers the ATO to bypass this step.

Much like a court-ordered garnishee, the ATO can seek to recover the outstanding debt you owe from employers, banks, financial institutions and other third parties. If you’re running a business, the order may also extend to merchant card and banking facilities as well as trade debtors.

You can read more about ATO garnishee orders here.

How to stop a garnishee order

There are a few ways to cancel or stop a garnishee order. Keep in mind that the strategy most likely to work for you will depend on your circumstances.

Pay the debt in full

If you can raise the money to pay the debt in full – do so, and the order will stop.

Make an alternative arrangement with the creditor

You may be able to negotiate with the judgment creditor. If the garnishee order is going to affect your ability to survive, there are options. You may be able to plead your case and ask the creditor to deduct a reduced amount instead.

The judgment creditor doesn’t HAVE to accept your proposed repayments. But they may consider it if you have a compelling reason to show you would otherwise face undue hardship.

Make an application to pay by instalments through the court

If the judgment creditor was unwilling to accept an alternative arrangement, you could apply to the court for an instalment order. You’ll need to lodge a statement of your financial position to support your application. If the court accepts your request, any enforcement action by the judgment creditor will be stayed. This means they can’t keep garnisheeing you or take other recovery measures on that debt.

You’ll need to ensure you don’t default on any court-approved instalment plan. If you do, the agreement may be cancelled and the judgment creditor will recommence their previous action.

If the court rejects your application to pay by instalments, it’s likely due to one of two reasons:

- It’ll take too long to repay the debt based on the amount you proposed or;

- You can’t afford the amounts offered – based on the financial statement you gave to the Court.

Utilise the Bankruptcy Act

The Bankruptcy Act will stop the garnishee order. It’ll also prevent the judgment creditor from taking further action against you. If you owe other provable unsecured debts, the bankruptcy act will also take care of these.

The available options within the Bankruptcy Act are;

To learn more about bankruptcy and how it might impact you, see what is bankruptcy and how bankruptcy might affect you.

If you’re currently dealing with a garnishee order and need some advice, call us now on 1300 369 168, start a chat, or make an online enquiry to speak with an expert.