While the numbers for Bankruptcy NSW rose during 2018, the east-coast state isn’t alone

According to the Australian Financial Security Authority (AFSA), the numbers for Bankruptcy NSW are up. Similarly, all bankruptcy administrations are reportedly up by 3%. This is the highest annual increase in bankruptcies since the GFC.

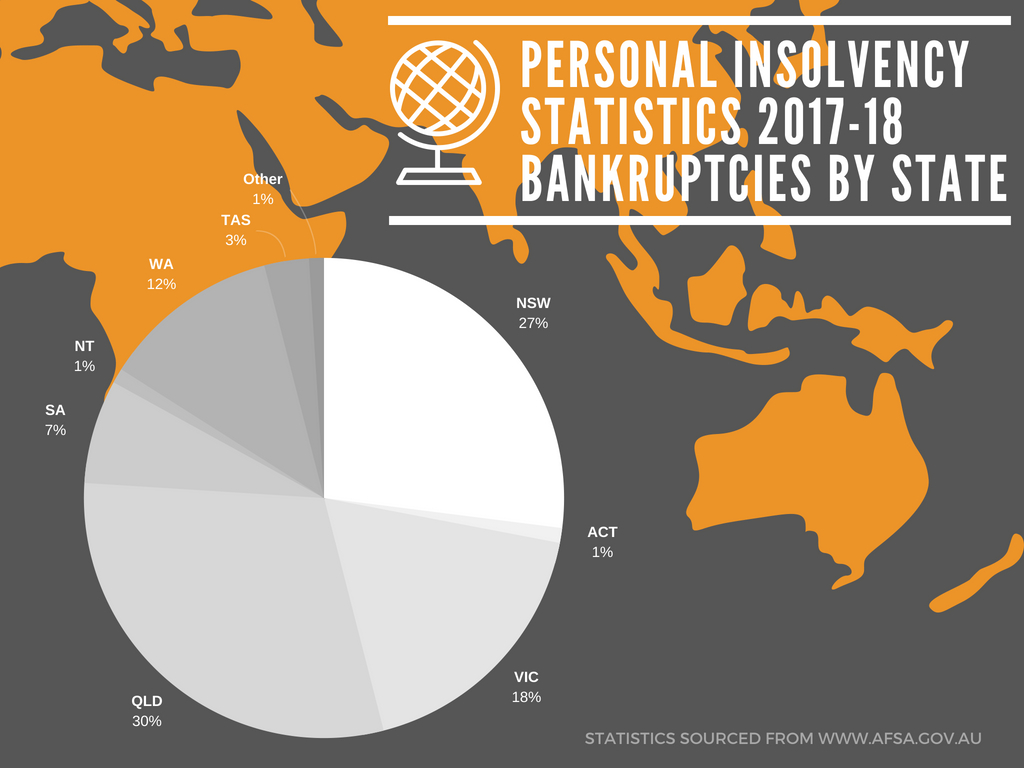

The rise was purportedly due to increases in the following states:

| Type of Administration & Where | Percentage Increase |

| Bankruptcy NT | 31.7% |

| Bankruptcy TAS | 11.0% |

| Bankruptcy WA | 10.6% |

| Bankruptcy NSW | 3.0% |

| Bankruptcy QLD | 2.9% |

| Bankruptcy SA | 0.6% |

These increases were offset by falls in:

| Type of Administration & Where | Percentage Decrease |

| Bankruptcy ACT | 5.6% |

| Bankruptcy VIC | 5.4% |

The Rising Numbers For Bankruptcy NSW

The increase is Bankruptcy NSW likely a result of many factors including a slowing property market, large levels of household debt, marginal wage growth and rising cost of living.

This is particularly relevant for Sydney, where median rental prices are at $1,040 per week in the inner-city suburbs. In this situation, we find that being over-extended on credit cards, personal loans, and tax debt is a bit like shaking an entire bag of salt onto an already painful wound.

In the case of Millennials (no ‘smashed-avo on toast’ jokes ahead, we swear) many were priced-out of the Sydney property market long ago. A lack of assets and savings will likely present a challenge to those owing more than $60,000 – $70,000 in unsecured debt. In our experience, lenders are often unwilling to restructure large unsecured debts without any security to lend against.

While the full effect of the Royal Banking Commission is yet to be realised, we’re likely to see lenders tighten their criteria across the board – leaving those with unmanageable unsecured debts very few options.

Statistical data sources from AFSA’s annual personal insolvency statistics

A 2016 study conducted by Experian found Millennials to display a “markedly different attitude to credit than the generations before them”. Millennials (21%) were reportedly three times more likely to use one type of credit product to pay off another, compared to the average GenX and Baby boomer (6.5%).

The study also found that one in four Millennial and GenX mortgage holders (26%) were extremely concerned about their ability to make mortgage repayments if their interest rate increase by 1.5%.

For those who managed to buy property in the inner-city and are currently servicing interest-only payments, there may be cause for concern. The eventual shift to principal and interest repayments could prove unmanageable for some and we may just see the numbers for Bankruptcy NSW climb again in 2019 & 2020.

Isn’t Bankruptcy The Worst Thing You Can Do?

Not always but it will depend on your situation.

While some aspects of the legislation are straightforward, others are more complicated.

Unfortunately, the complicated parts are often explained by way of “sweeping statements”. In our experience, such statements often fall short of educating consumers on the ins and outs of how bankruptcy works. Instead, they often contribute to misinformation and the continuing stigma surrounding this subject.

Bankruptcy basics

Some of the more straightforward aspects of bankruptcy are:

- It’ll clear unsecured, provable debts like credit cards, personal loans, overdrafts, property or vehicle shortfalls, and most tax debts

- The bankruptcy will typically last for 3 years and 1 day

- There’ll be a notation on your credit report for two years after you’re discharged. This means that your credit report will only be impaired for 5 years in most cases. While the government keeps a permanent record of the bankruptcy (NPII), it’s held separately from your credit record

- Your standard household contents and super are generally protected

- You’re unable to be the director of a company during bankruptcy – unless you obtain consent from the court. But, you’re allowed to operate a business as a sole trader or as a partnership – provided that partnership is created after the date of bankruptcy as any pre-existing partnerships will be dissolved

- You’ll need permission to travel overseas while you’re bankrupt but it’s easy to do this if you’re playing by the rules

Bankruptcy not-so-basics

Figuring out how income is assessed or what happens to certain assets is where many people start to struggle.

Income

Heard this phrase before?

“You can only earn $1000 and then everything else is taken”

Although it couldn’t be further from the truth, we’ll often hear people innocently parroting this “sweeping statement” because a backyard expert (or the like) told them so… and surely they must be right, right?

In the case of income, a statutory formula set out in the Bankruptcy Act determines the assessment of income. Whether you have to make payments will depend on how much you’re earning and the number of dependants you support. and whether you’re receiving any fringe benefits or salary packaging will also determine what you pay.

Let’s review a super basic example of how income contributions are calculated in bankruptcy.

If you’re earning around $90,000 gross taxable per year, have no dependants, child support payable or any other components to your income such as fringe benefits or salary sacrifice, here’s how your income might be assessed:

| Gross Taxable Income: | $90,000.00 |

| Less Tax Payable: | $27,762.00 |

| = Assessable Income: | $67,238.00 |

| Less the threshold for no dependants | $56,674.80 |

| = Excess above the threshold: | $10,563.20 |

| Amount payable per year (Excess ÷ 2): | $5,281.60 |

| Amount payable per week (Annual ÷ 52): | $101.57 |

In the above example, you’d need to pay around $100 per week towards your bankrupt estate. The rest of your pay (almost $1,200) would then be yours to keep.

Take that, John Snow.

Click here to read more about income contributions during bankruptcy.

Assets

Property can also be a confusing and daunting topic for most people. Bankruptcy protects some assets and not others. In the biz, we call these unprotected assets “vested” or “vesting” property.

Some examples of unprotected or vesting property are:

- Real property such as houses and units;

- Vehicle assets worth more than the protected threshold (currently $7,900). If your vehicle is under finance, this threshold applies to the equity in the vehicle;

- Shares, stocks, bonds and cryptocurrency and;

- Caravans, boats, and trailers

Once you become bankrupt, your ownership of any vested assets will shift to your bankruptcy trustee.

Your trustee will need to realise the value of your interest in any vesting assets in order to make those funds available to your bankrupt estate. Contrary to popular belief, it can sometimes be possible to do this without selling the asset to a stranger. For example, instead of putting your property on the open market, a trustee may look to sell your interest in the unprotected asset(s) to a non-bankrupt third party, such as a co-owner, at market value.

We cover how this process can sometimes work in further detail here.

Truth is, the Bankruptcy Act is a big piece of legislation that can’t be explained in a couple of sentences. To understand how it will affect you, you’ll need to put the legislation into the context of your individual situation.

Given the above, it’s important for consumers to be savvy when conducting their research. You should maintain a healthy level of scepticism when faced with “sweeping statements”. Particularly if they’re in lieu of clear explanations of how certain aspects of bankruptcy work.

[From left to right: Alexander Clark – Registered Trustee, Andrew Aravanis – Registered Trustee and Ronil Roy – Registered Trustee]

If you’re currently struggling with debt and need further information on bankruptcy, call us now on 1300 369 168, start a chat, or make an online enquiry to speak with an expert.