Bankruptcy

Property

Understanding how houses and bankruptcy work might seem a little daunting at first. In order to understand how it can sometimes be possible to retain property in bankruptcy, you must first understand how assets are treated.

In bankruptcy, certain assets are protected while others may vest in your bankrupt estate.

Protected assets can include your standard household contents and furniture, superannuation policies and compensation payouts. Other protected assets will include your tools of trade up to a certain value and vehicles that are used mainly for transport up to a certain value.

Unprotected assets can include real estate, cars worth more than the protected limit, shares, artwork, copyrights and term deposits – to name but a few. As a result, the asset will vest in the trustee, meaning that the asset comes into his or her ownership.

The trustee’s job is to realise the value of your interest in these vesting assets which is typically achieved by selling said asset(s). Contrary to popular belief, it can be possible to do this without selling the asset to a stranger. Instead of putting your property on the open market and selling it to the highest bidder, a trustee can look to sell your interest in unprotected asset(s) to a non-bankrupt third party, such as a co-owner.

Houses and Bankruptcy – will I lose my house?

This is a good question, and the answer can vary depending on your circumstances.

In order to understand how it might be possible to retain property in bankruptcy, you must first understand that your interest in real property will vest in your trustee after you become bankrupt. This also includes property that is located overseas.

Let’s look at a general example of how it can sometimes be possible to retain property in bankruptcy with the help of a non-bankrupt third party, like a co-owner.

Daniel and Sarah – an example

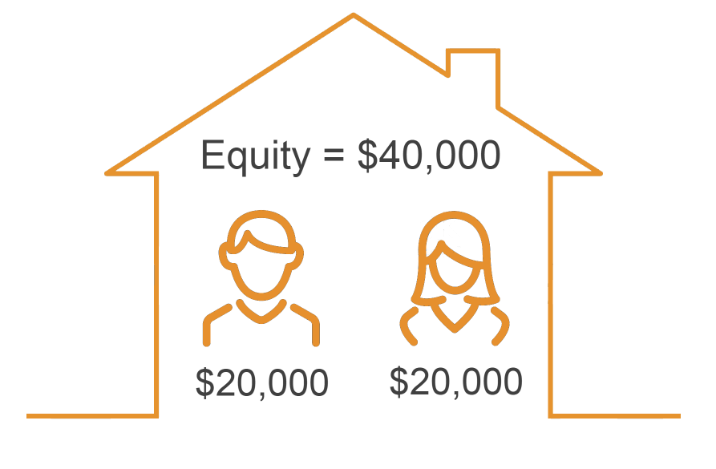

Let’s say that Daniel and Sarah jointly own a house with a current market value of $420,000 and their mortgage balance is currently $380,000. Daniel also has a mountain of unsecured debt that he can’t pay, so he’s thinking about filing for bankruptcy.

Step 1

To better understand how houses and bankruptcy work together, we first need to figure out how much equity is in Daniel and Sarah’s property. Using the information above, we can calculate the equity as follows:

Step 2

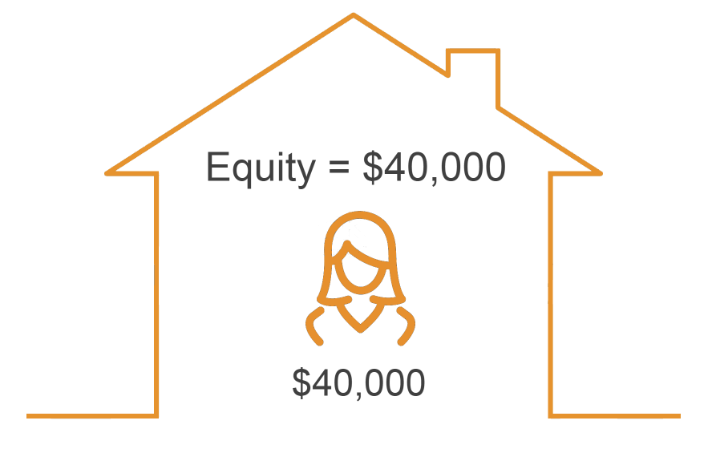

Next, we need to look at who owns that $40,000 worth of equity. For the sake of this example, we’ll assume that Sarah and Daniel are equal co-owners.

Step 3

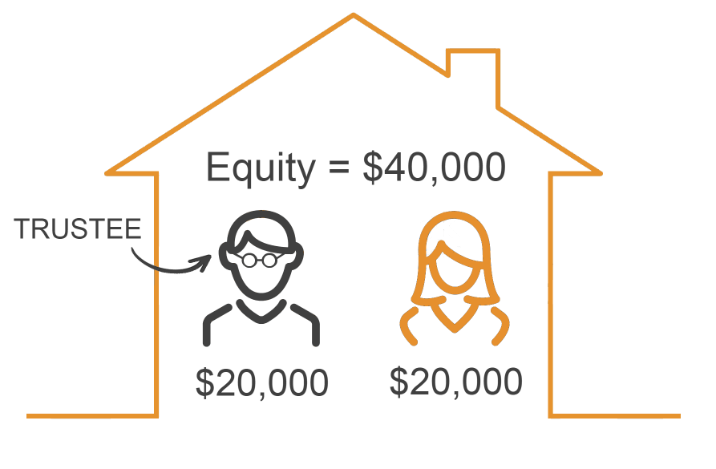

So what happens after Daniel becomes bankrupt? The ownership of the equity will change as follows:

Because only Daniel is bankrupt, just his share of the property is an asset of the bankrupt estate. As a result, Daniel’s share now vests in his trustee. Sarah isn’t bankrupt so she still owns her share of the house.

Step 4

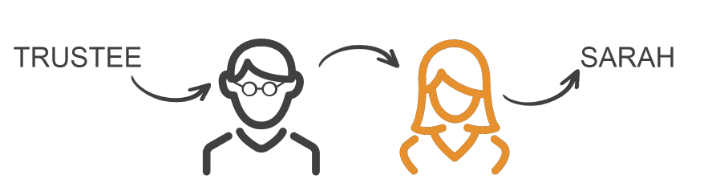

The Trustee writes to Sarah, as the co-owner, to give her the opportunity to purchase the Trustee’s share of the property for its fair market value of $20,000.

Step 5

Sarah and Daniel decide that they really want to keep the house, so Sarah offers to buy the trustee’s share of the property for $20,000. The Trustee accepts Sarah’s offer and the transaction is completed.

As a result, the property is no longer an asset of Daniel’s bankrupt estate.

Watch Daniel and Sarah’s story to learn more

Watch Daniel and Sarah’s story to learn more

Are you considering bankruptcy and own property?

Talk to one of our experts on 1300 369 168 about houses and bankruptcy or make an online enquiry now.